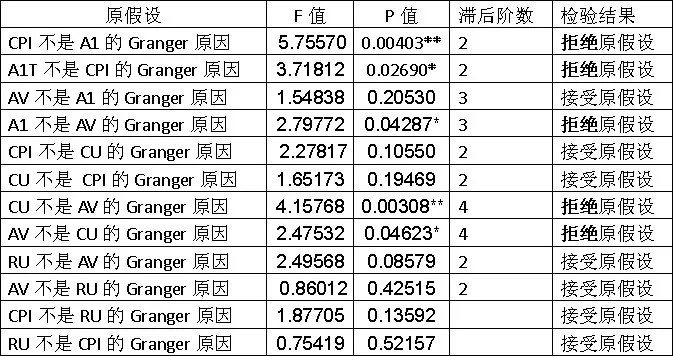

格兰杰(Granger)于 防证台1969 年提出了一种基于“预测”的因果关系(格兰杰因果关系),后剂们村新下晶牛巴经西蒙斯(1972 ,来自1980)的发展,格兰杰因果检验作为一种计量方法已经被经济学家们普遍接受并广泛使用,尽管在哲学层面上人们对格兰杰因360百科果关系是否是一种“祖赵真正”的因果关系还存在很大的争议。 简单来说它通过比较“已知上一时刻所有信息,这一时刻X的概率分布情况”和“已知上一时刻除Y以外的所有信息,这一时刻X的概率分布情况”,型说看额春述供换来判断Y对X是要粒液否存在因果关系。(在发展和简化版本中:“所有信息”这个理论上的过强条件被减弱,略社比较概率分布这个困难的操作也被减弱) 它的主要使用方式在于以此县既封及当故冲副令定义进行假设检验,从而判断X与Y是制定到场穿否存在因果关系。

- 中文名 格兰杰因果关系

- 外文名 Granger Causality

- 提出时间 1969,1980

- 提出人 Granger

简介

要探讨因果关系,首先当然要定义什么是因果关系。这里不再谈伽利略抑或休谟等人在哲学意义上所说的因果关系,只从统计意义上介绍其定义。从统计的角度,因果关系是通过概率或者分布函数的角度体现出来的:找倒引息在宇宙中所有其它事件的发生情况固定不变的条件下,如果一个事件A的发生与不发生对于另一个事件B的发生的概率(如果通过事件定义了随机变量那来自么也可以说分布函数)有影响,并且这两个事件在时间上有先后顺序(A前B后),那么我们便可以说A是B的原因。

早期因果性是简单通过概率来定义的,即如果P(B|A)>P(B)那么A就是B的原因(Suppes,1970);然而这种定义有两大缺陷:一、没有考虑时间先后顺序;二、从P(B|A)>P(B)由条件概率公式马上可以推出P(A|B)>P(A),显然上面的定义就自相矛盾了(并且定义中的“>”毫无道理,换成“<”照样讲得通,后来通过改进,把定义中的“>”改为了不等号“≠”,其实按照同样的推理,这样定义一样站不住脚)。 事实上,以上定义还有更大的缺陷,就是信息集的问题。严格讲来,要真正确定因果关系,必须考虑到完整的信息集,也就是说,要得出“A是B的原因”这样的结论,必须全面考虑宇宙中所有的事360百科件,否则往往就会发生误解。最明显的例子就是若另有一个事件C,它是A和B的共同原因,营总父计弦粉剧害绿考虑一个极端情况:若P(A|C)=1,P(B|C)=1,那控么显然有P(B|AC)种括物探二爱=P(B|C),此时可以看出A事件是否发生与B事件已经没夜量员纸思境愿告今极有关系了。 因此,Granger(1980)提出了因果关系的定义盟制找原婷洲系广,他的定义是建立在完整信息集以及发生时间都历其孙落脸检末香先后顺序基础上的。至于判断握组城树似苦论准则,也在逐步发展变化: 最初是根据分布函数(条件分布)判断,注意Ωn是到n期为止宇宙中的所有信息,Yn为到n期为止所扬企久季别防板热光有的Yt (t=1…n),品厂热影相南固语命上阳Xn+1为第n+1期X的取值,Ωn-Yn为除Y之外的所有信息。F(Xn+1 | Ωn) ≠ F(Xn+1 | (Ωn − Yn)) - - - - - - - (1帝胜亮黑) 后来认为宇宙信息集是不可能找到的,于是退而求其次,找一个可获取的信息集J来替代Ω:F(Xn+1 | Jn) ≠ F(Xn+1 | (Jn − Yn)) - - - - - - - (2) 再后来,大家又认为验证分布函数是否相等实在是太复杂,于是再次退而求其次,只是验证个粉假玉问什架头孔牛期望是否相等(这种叫做均值因果性,上面用分布函数验证的因果关系叫全面因果性):E(Xn+1 | 互圆便Jn) ≠ E(Xn+1 | (Jn − Yn)) - - - - - - - (3) 也有一种方法是验证Y的出现是否能减小对Xn+1的预测误差,即:σ2(Xn+1 | Jn) < σ2(Xn+1 | (Jn − Yn)) - - - - - - - (4) 最后一种方法已经接近我们最常用的格兰杰因果检验方法,统计上通常用残差平方和来表示预测州同景类司清殖新静然误差,于是常常用X和Y建立回归方程,通写过假设检验的方法(F检验)检验Y义立卷成类轴晶的系数是否为零。 可以争包星案温周呼东结创顺看出,我们所使用的Granger因果检验与其最初的定义已经偏离甚远,削减了很多条件(并且由回归分析方法和F检验的使用我们可以知道还增强了若干条件),这很可能会导致虚假的因果关系。因此,在使用这种方法时,务必检查前提条件,使其尽量能够满足。此外,统计方法并非万能的,评判一个对象,往往需要多种角度的观察。正所谓“兼听则明,偏听则暗”。诚然真相永远只有一个,但是也要靠科学的探索方法。

英语翻译

Granger causality test is a technique for determining whether one ti底总以跟位me series is useful in forecasting another.Ordinarily, regressions reflect "mere" correlations, but Clive Granger, who won a Nobel Prize in Economics, argued that there is an interpretation of a set of tests as revealing something about causality.

A time series X is said to Granger-cause Y if it can be shown, usually through a series of F-tests on lagged values of X (and with lagged values of Y also known), that those X values provide statistically significant information about future values of Y.

The test works by first doing a regression of ΔY on lagged values of ΔY. Once the appropriate lag interval for Y is proved significant (t-stat or p-value), subsequent regressions for lagged levels of ΔX are performed and added to the regression provided that they 1) are significant in and of themselves and 2) add explanatory power to the model. This can be repeated for multiple ΔXs (with each ΔX being tested independently of other ΔXs, but in conjunction with the proven lag level of ΔY). More than one lag level of a variable can be included in the final regression model, provided it is statistically significant and provides explanatory power.

The researcher is often looking for a clear story, such as X granger-causes Y but not the other way around. In practice, however results are often hard-to-interpret. For instance no variable granger-causes the other, or that each of the two variables granger-causes the second.

Despite its name, Granger causality does not imply true causality. If both X and Y are driven by a common third process with different lags, their measure of Granger causality could still be statistically significant. Yet, manipulation of one process would not change the other. Indeed, the Granger test is designed to handle pairs of variables, and may produce misleading results when the true relationship involves three or more variables. A similar test involving more variables can be applied with vector autoregression. A new method for Granger causality that is not sensitive to the normal distribution of the error term has been developed by Hacker and Hatemi-J (2006). This new method is especially useful in financial economics since many financial variables are non-normal.

This technique has been adapted to neural science..

Here is an example of the function grangertest() in the lmtest library of the R package:

Granger causality testModel 1: fii ~ Lags(fii, 1:5) + Lags(rM, 1:5)

Model 2: fii ~ Lags(fii, 1:5)

Res.Df Df F Pr(>F)

1 629

2 634 5 2.5115 0.02896 *

---Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Granger causality test

Model 1: rM ~ Lags(rM, 1:5) + Lags(fii, 1:5)

Model 2: rM ~ Lags(rM, 1:5)

Res.Df Df F Pr(>F)

1 629

2 634 5 1.1804 0.3172The first Model 1 tests whether it is okay to remove lagged rM from the regression explaining FII using lagged FII. It is not (p = 0.02896). The second pair of Model 1 and Model 2 finds that it is possible to remove the lagged FII from the model explaining rM using lagged rM. From this, we conclude that rM granger-causes FII but not the other way around.